Jakarta, 30 October 2025 - Indonesia’s economy is likely to have maintained steady growth during Q3 2025. Recent indicators suggest year-on-year growth remains around 5%, relatively unchanged from the previous quarter. Household consumption has stabilized, while investment continues to be the main driver of recovery, although we are unlikely to see the extent of lift seen in the previous quarter. Fiscal spending is expected to pick up toward the end of the year, providing an additional boost to growth.

Overall, high-frequency data show that the economy remains stable. Demand patterns remain solid but uneven across sectors, influenced by structural factors and sentiment adjustments. Growth risks appear slightly tilted upward, depending on the realization of investment in the government’s official report.

Household Consumption: Caution Remains

Household consumption, which accounts for more than half of GDP, continues to be the main determinant of quarterly growth. In September 2025, retail sales rose by 5.84% (yoy), the fastest pace since early 2024. This improvement provides some relief after a sluggish start to the year when household demand was pressured by weak confidence and limited income growth.

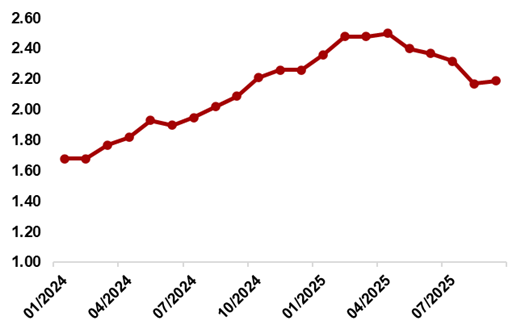

Fig 1. Core CPI Inflation Remains Subdued

{kind=link}

Even so, the rebound appears less than robust. Core inflation averaged only 2.2% yoy in Q3 indicating that the underlying momentum in spending remains subdued. In theory, stable core inflation points to sound price control. In practice, it also reveals modest purchasing power growth and the absence of strong demand pressures.

Consumer confidence has not shown significant recovery. Index data suggest households remain cautious, indicating unstable sentiment. This is partly due to structural issues such as slow income recovery in the informal sector, and cyclical factors like economic fatigue and uncertainty about future living costs.

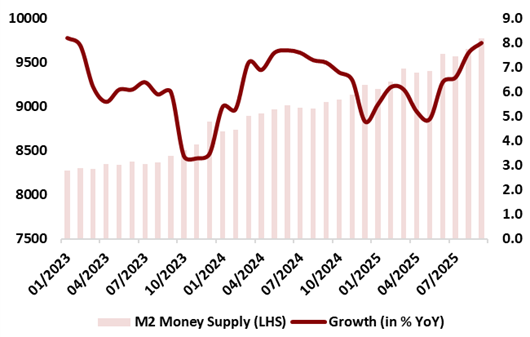

There are, however, tentative signs of improvement in liquidity. Broad money supply (M2) rose 8% yoy in September, rebounding from the lows seen in Q2. This improvement points to a more effective monetary transmission, helped by the government’s liquidity placements in banks and ongoing easing by Bank Indonesia (BI). Since June 2024, BI has cut its policy rate by 150 basis points, creating a more accommodative environment for credit and spending.

Fig 2. Broad Money M2 Rebounded from Q2

The effect of easier liquidity is gradual. Theoretical relationships between money growth and nominal income suggest that sustained M2 expansion can eventually lift consumption, though the current gap between liquidity and spending growth remains narrow. For now, the recovery in household expenditure looks steady but not strong, supported more by stabilization than acceleration.

Overall, household consumption in Q3 is likely to record slightly higher growth than in Q2, partially due to a low base effect but also as an early result from improved liquidity conditions. However, the general economic recovery remains cautious, reflecting a normal adjustment phase rather than a burst of optimism.

Fiscal Dynamics: Room for a Year-End Push

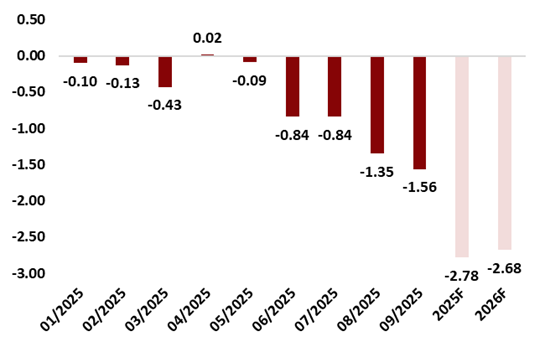

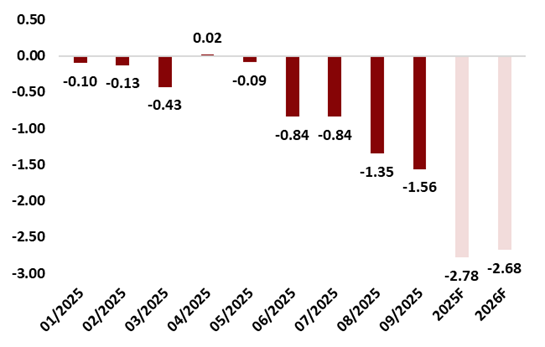

Fiscal policy remains a key stabilizer, though execution has been slower than planned. As of September 2025, the rolling budget deficit stood at 1.56% of GDP, leaving wide room below the official full-year target of 2.78%. This indicates that the government still holds ample fiscal space to accelerate spending in the final quarter.

Fig 3. Rolling Budget Deficit Still Off-Target

{kind=link}

By the end of September, central government spending had reached only 59.7% of the annual target, compared to 64.7% during the same period last year. This low realization shows that fiscal support during Q3 was still limited but also opens the door for a year-end spending surge as ministries typically rush to absorb budgets.

From a macro perspective, higher fiscal outlays inject liquidity and confidence through several channels. Direct spending raises incomes and employment, particularly in construction and services. Improved cash flow encourages private credit creation. Stronger local transfers sustain regional economies that depend heavily on central funding.

This momentum is further supported by coordinated fiscal-monetary policy. With BI maintaining an accommodative stance, additional government spending should reinforce growth without stoking inflation. If disbursement accelerates as planned, it could add 0.1–0.2 percentage point to full-year GDP growth. The outcome, however, will hinge on execution efficiency and absorption capacity within key ministries.

Investment: Strength with Signs of Plateauing

In Q2, investment delivered its strongest contribution in several years. However, Q3 data indicate that the momentum has begun to moderate.

Imports of capital goods, a leading indicator of investment activity, grew 32.5% year-on-year in Q2 but slowed to around 11.2% in July–August. This moderation implies that several large projects have entered later stages or paused pending new approvals.

Fig 4. Credit Growth (YoY) Remains Single-Digit

The banking sector shows a similar pattern. Credit growth fell from 13.1% in April 2024 to 7.6% in September 2025, reflecting weaker loan demand from corporations adjusting to slower orders and households holding back on consumer borrowing. Some of the mid-year uptick in lending was linked to the government’s IDR 200 trillion placement in Himbara banks, which temporarily boosted credit flows but did not alter the underlying trend.

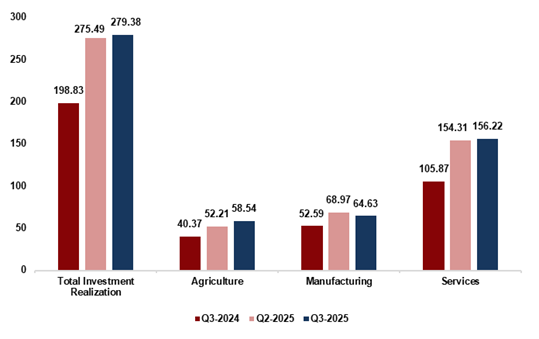

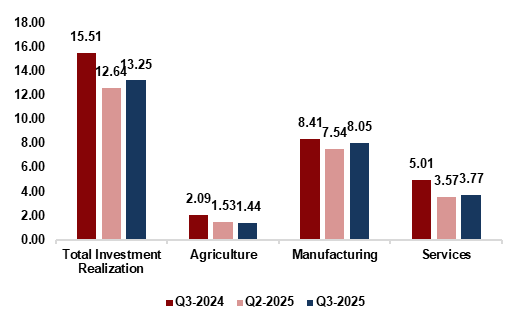

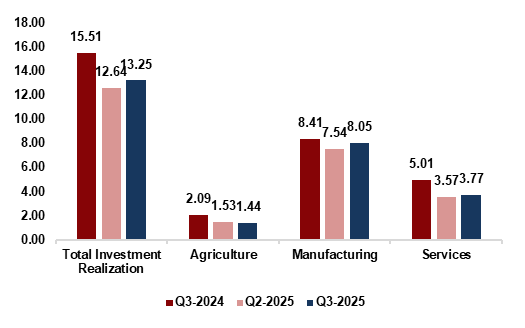

Still, headline investment numbers remain encouraging. According to BKPM, investment realization grew 13.9% year-on-year in Q3, up from 11.5% in Q2. Both foreign and domestic investment rose on a quarterly basis, with the services sector—including data centers, logistics, and digital infrastructure—absorbing the bulk of inflows. The manufacturing sector, by contrast, experienced a mild decline, underscoring concerns about premature deindustrialization amid a growing tilt toward services and resources.

Fig 5a. Domestic Investment Realization (IDR tn)

Fig 5b. Foreign Investment Realization (USD bn)

{kind=link}

This structural change carries policy implications. While service-based investment supports short-term resilience, Indonesia’s long-term competitiveness will depend on strengthening industrial capacity. Clear policy direction and stronger supply chains are needed to sustain manufacturing momentum.

Overall, investment remains a key determinant of Q3 GDP. If realization aligns with BKPM data, investment could again support growth at the upper bound of expectations. If not, headline growth will likely settle around 5.0%.

External Sector: Cushioning, Not Driving

The external environment remains supportive, though it no longer defines the growth narrative. Indonesia’s trade surplus has persisted, cushioning the economy against domestic fluctuations.

In August 2025, the surplus reached USD 5.49 billion, the highest since early 2024. Exports stayed positive through the year, albeit at a slower pace. Import growth, driven largely by capital and intermediate goods, mirrors continued domestic investment.

Major export destinations—including China, India, and the United States—maintained PMIs in expansionary territory, signaling resilient external demand. Only Japan registered a contraction due to weaker manufacturing output. This geographic spread helps Indonesia diversify risk and maintain steady export receipts.

Commodity prices remain the principal variable. Coal and crude palm oil (CPO) prices rose between July and August, boosting export earnings. By September, coal prices had softened, but firmer CPO prices offered partial offset. These fluctuations are manageable; Indonesia’s broad commodity base ensures that losses in one area are often cushioned by gains in another.

From a macro standpoint, exports now contribute less than one-quarter of GDP, meaning that external trade plays a supportive rather than dominant role. Even so, the sustained surplus helps stabilize the rupiah, strengthens foreign reserves, and increases non-tax revenues—all crucial for maintaining fiscal flexibility. Going forward, global commodity trends and inventory cycles will shape external performance. For now, the external balance remains a reliable buffer, cushioning any softness in domestic investment or consumption.

Policy Mix and Macroeconomic Context

The policy environment remains broadly supportive. Bank Indonesia’s monetary easing since 2024 has improved liquidity without triggering capital outflows or exchange-rate instability. The rupiah has been relatively stable, reflecting credible macro fundamentals and a healthy balance of payments.

On the fiscal front, the government’s early-year restraint has created room for a stronger end-year push. This coordination between fiscal and monetary sides has kept financing costs low while sustaining growth momentum.

In theoretical terms, Indonesia’s current policy stance represents a coordinated expansion within prudential limits. Monetary easing ensures liquidity, fiscal measures sustain demand, and external stability provides policy space. This configuration supports a sustainable 5% growth trajectory, even without a sharp cyclical rebound.

The challenge now is qualitative rather than quantitative. Sustaining 5% growth is achievable; lifting it beyond 5% requires a revival in private confidence, stronger productivity gains, and deeper structural reform.

Conclusion

The forthcoming Q3-2025 GDP release will likely confirm another quarter of steady 5% growth, consistent with Indonesia’s current medium-term potential. Within the composition, investment should remain the main contributor, private consumption should edge slightly higher, and net exports should continue to provide a modest cushion.

Upside risks stem from stronger investment realization and faster government spending in Q4. Downside risks arise from continued household caution and slow project execution.

Overall, Indonesia’s economy remains on a stable and measured path—neither overheated nor weak. The macroeconomic foundation is strong, coordination between monetary and fiscal policies is shaping up rather well, and the growth base is broad enough to withstand global volatility. The next challenge is transforming this stability into productivity gains, stronger private confidence, and a reinforced industrial base. Only then can Indonesia move from stable 5% growth toward a higher and more sustainable trajectory.